August 16, 2022 |9 min read August 16, 2022 |9 min

read Credit scores are used to predict how likely a person is to pay their loans and credit card bills on time. That’s simple enough. But trying to explain what a good score is can be more difficult. If you’re just looking for a quick answer, it’s probably best to start with popular credit-scoring companies FICO® and VantageScore®, which issue

two of the many different types of credit scores. But there’s a lot more to it than that. So keep reading to take a closer look at credit scores, including how they’re determined, who’s looking at them, and what you can do to monitor and improve yours. Key Takeaways Good Credit BasicsIt may help to establish a few things about credit scores before going any further. According to the Consumer Financial Protection Bureau (CFPB), scores are typically based on information from your credit reports. And they’re calculated by companies like FICO and VantageScore using complex formulas called scoring models. The following video explains a little more about how credit works: Why Are There Different Credit Scores?Credit-scoring companies use different methods to calculate credit scores. And they might weigh information in your credit reports differently as part of their calculations. That’s why your scores are likely to vary, even if just by a few points, when you compare them. What’s a Good Credit Score Range?A good credit-score range depends on where a score comes from, who calculates the credit score and who’s judging it. It’s important to remember that lenders set their own credit policies and standards to determine creditworthiness. That means that what FICO, VantageScore or anyone else considers good may not be the same. However, there are some general guidelines for how being within a score range can impact your choices:

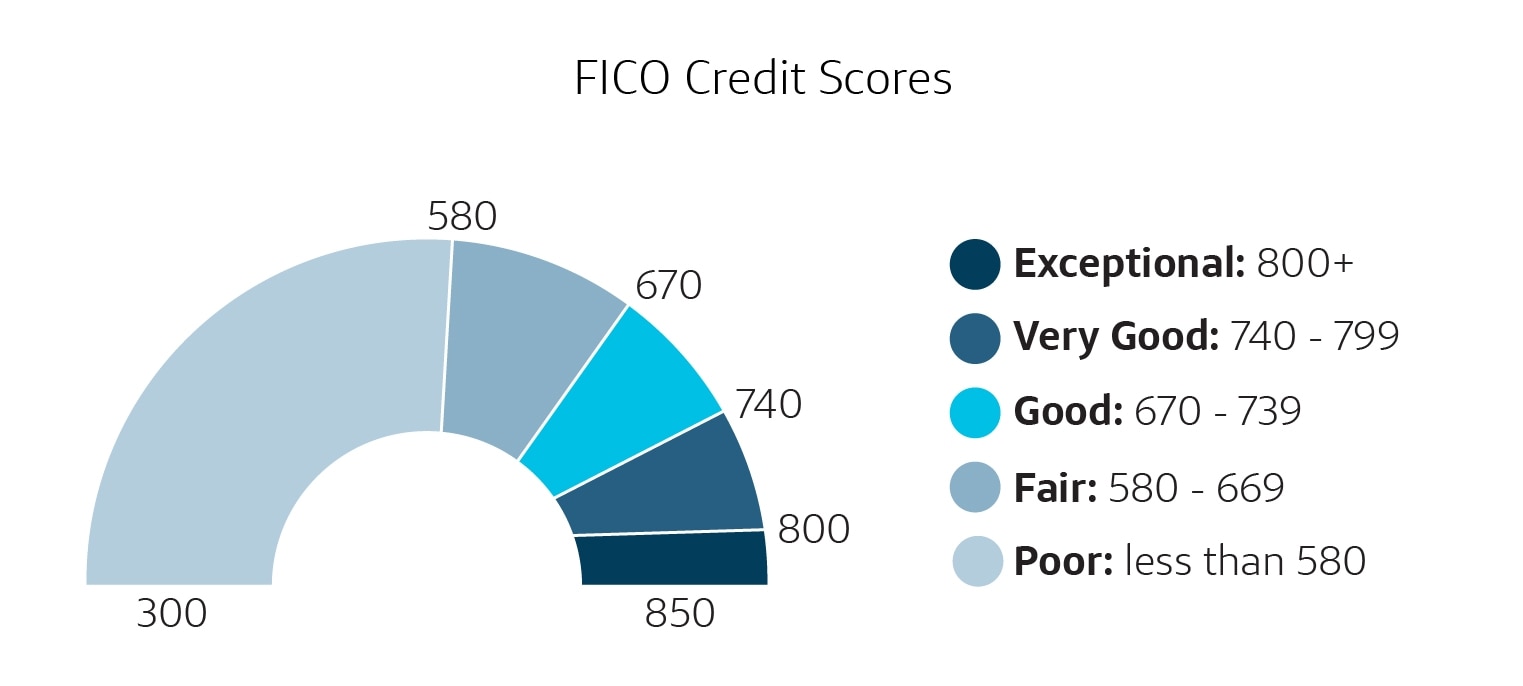

What’s a Good FICO Credit Score Range?Originally Fair, Isaac and Company, FICO helped standardize credit scoring. That was in 1989. In the 30-plus years since, FICO has created multiple versions of its scoring models. But it says today’s models are still very similar to the original. FICO scores that range between 670 and 739 qualify as good scores. Scores in that range are near or slightly above the U.S. average. In total, FICO breaks its scores into five categories: What’s a Good VantageScore Credit Score Range?VantageScore entered the picture in 2006. It’s managed independently, but it was founded by Equifax®, Experian® and TransUnion®, the three major credit bureaus. In addition to FICO scores, lenders may rely on VantageScore credit scores to judge things like loan or credit applications. And VantageScore credit scores can be found in free monitoring services like CreditWise from Capital One. You can also learn how to get free copies of your credit reports by visiting AnnualCreditReport.com. When it comes to VantageScore, scores between 661 and 780 might be considered good. VantageScore also breaks its scores into five groups, but uses different ranges and naming conventions than FICO: What Affects Your Credit Scores?So you can see credit-scoring models and credit reports are two big factors that determine your credit score. But if you don’t know what information from your credit report is being used, it’s not much help. Here are a few factors the CFPB says make up a typical credit score:

How Does FICO View Those Credit Factors?FICO is pretty specific about what it views as the most important credit factors. Payment history makes up about 35% of its scoring. About 30% is based on the total debt. The other primary factors are credit history (15%), credit mix (10%) and new credit (10%). These percentages can vary depending on what’s in your credit report, but they’re a good general guide. How Does VantageScore View Those Credit Factors?VantageScore doesn’t give percentages. But it’s clear about what’s crucial to its scoring models. It says credit utilization is extremely influential. Credit mix and experience are highly influential. Payment history is moderately influential. And credit age and new credit are less influential. What Information Do Credit Scores Not Consider?Most credit-scoring models don’t consider information unless it’s part of your credit report. And even then, some parts of your credit report don’t impact your scores. FICO's and VantageScore’s scoring models don’t consider:

Closed and paid-off accounts will stay on your credit reports and can continue to impact your scores until they fall off. What Is a Good Credit Score for My Age?Your age doesn’t directly influence your credit scores. But as FICO and VantageScore show, the age of your credit accounts is one factor that affects how scores are calculated. That could be one reason people’s credit scores tend to increase as they get older—their accounts have simply been open longer. But credit scores can rise or fall no matter how old you are. And having good credit scores comes down to more than just the age of your accounts. Why Is a Good Credit Score Valuable?Now you know a little more about where scores come from. But that doesn’t explain why good credit scores are so valuable. Credit scores are often associated with credit risk, credit cards, loan applications and other lending decisions. And having a good score could help you qualify for more financial products with better rates, terms and credit limits. But the influence of credit scores goes beyond that. And even when you’re not borrowing money, good credit could help you. Good scores could lead to lower insurance rates and fewer and lower security deposits on things like telecom and utility accounts. And good scores may make it easier to rent a home, too. Your credit reports—but not your scores—could even impact some job prospects. Pre-Approval, Pre-Qualification and Comparing OffersFor starters, you may be pre-approved or pre-qualified for more credit offers if you have good credit scores. That may allow you to compare offers and find the best fit for your situation—whether you’re looking at mortgages, credit cards or auto loans. But if you’re shopping around, be sure to understand how credit inquiries can affect your credit scores. Interest Rates and Credit LimitsIf you’re approved for a loan or a credit card, a good credit score could mean higher credit limits, lower interest rates or both. And when you’re paying less in interest, you may have smaller payments and be able to pay off debt faster. In general, that means that higher credit scores could decrease the cost of borrowing money. Beyond Credit Cards and LoansGood credit could affect other parts of your life, too:

How to Build a Good Credit ScoreBuilding a good credit score comes down to using credit responsibly over time. The same is true when it comes to maintaining a good credit score. Here are five things the CFPB says you can do:

Credit Score FAQsHow Can You Start Building Credit History?There are a number of products to help customers who may be new to credit or trying to rebuild their credit. Many people start with a secured credit card, student credit card, credit-builder loan or student loan. Is It Possible to Improve Your Credit Scores Quickly?Building good credit can take time, but there are steps you can take to help improve your credit scores. If you have a high credit utilization ratio that’s hurting your credit scores, paying down your revolving credit account balances might quickly improve your scores. Or if there’s incorrect negative information in your credit report, disputing the error and getting it corrected right away could help. Why Did My Credit Scores Change?It’s common for scores to change somewhat throughout the month as creditors send the bureaus new or updated information about accounts. But figuring out what exactly caused the changes can be difficult. If your scores suddenly dropped after you missed a couple of payments, you could assume that might have been the cause. But a slight increase or decrease could also be a normal result of your accounts aging—or new payments or updated balances being added to your credit report. You may also see different scores depending on where you check your credit. Remember, scores depend on both the scoring model used and the credit report that the scores analyze. There are many different versions of FICO and VantageScore. And according to the CFPB, some lenders have their own custom credit-scoring models that they use to make credit decisions. But in general, your credit scores get created as a snapshot of your credit report when they’re requested. So any changes in the underlying credit report could lead to changes in scores. Good Credit Scores in a NutshellUsing credit accounts and paying your bills on time can help you establish credit and lead to good—and even very good or excellent—credit scores. And avoiding late payments and having low credit card balances could also help you maintain good credit. You can also consider using a credit-monitoring service, like CreditWise, to keep an eye on what’s in your credit reports and where your credit scores stand. We hope you found this helpful. Our content is not intended to provide legal, investment or financial advice or to indicate that a particular Capital One product or service is available or right for you. For specific advice about your unique circumstances, consider talking with a qualified professional. Capital One does not provide, endorse or guarantee any third-party product, service, information, or recommendation listed above. The third parties listed are solely responsible for their products and services, and all trademarks listed are the property of their respective owners. Your CreditWise score is calculated using the TransUnion® VantageScore® 3.0 model, which is one of many credit scoring models. It may not be the same model your lender uses, but it can be one accurate measure of your credit health. The availability of the CreditWise tool depends on our ability to obtain your credit history from TransUnion. Some monitoring and alerts may not be available to you if the information you enter at enrollment does not match the information in your credit file at (or you do not have a file at) one or more consumer reporting agencies. August 16, 2022 |9 min read Related Contentarticle | September 29, 2022 | 8 min read article | January 16, 2020 | 8 min read article | March 29, 2022 | 7 min read What is a good credit score for my age?Anywhere between 670 to 739 is considered good. A credit score between 740 to 799 is considered very good. Credit scores 800 and up are considered excellent. Someone with a VantageScore that's 600 or less is considered to have poor or very poor credit.

How do I know if my credit is good?Lenders may use credit scores to evaluate loan qualification, credit limit and interest rate. For a score with a range between 300 and 850, a credit score of 700 or above is generally considered good. A score of 800 or above on the same range is considered to be excellent.

What credit score do most look at?When it comes to credit scores, however, there is a clear winner: FICO® Score is used in 90% of lending decisions. It's crucial that consumers understand at least the basics of how credit reports work and credit scores are calculated.

How do I get my credit score from 750 to 800?How to Get an 800 Credit Score. Pay Your Bills on Time, Every Time. Perhaps the best way to show lenders you're a responsible borrower is to pay your bills on time. ... . Keep Your Credit Card Balances Low. ... . Be Mindful of Your Credit History. ... . Improve Your Credit Mix. ... . Review Your Credit Reports.. |

What does a good credit score look like

Related Posts

Copyright © 2024 paraquee Inc.